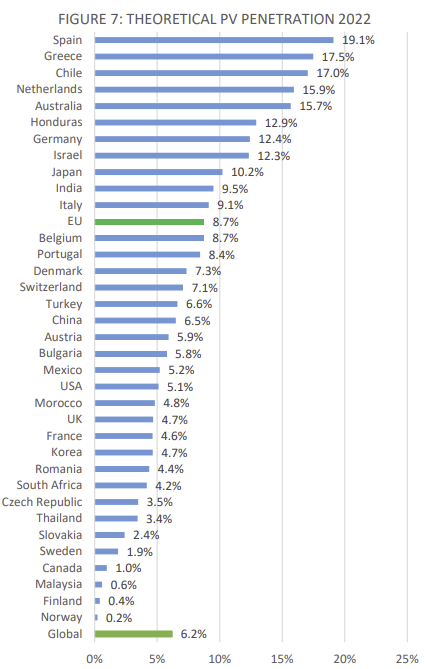

According to the balance sheet of the International Energy Agency for the global solar market in 2022, Greece recorded the second highest rate of infiltration of photovoltaic plants, after Spain. Specifically, Spain is in the top with 19.1%, followed by Greece in the second place with 17.5% and Chile in the third place with 17.0%. These figures indicate that photovoltaic systems are theoretically contributing to meeting energy demand in several markets, based on installed capacity at the end of 2022.

According to the report, the figures presented are estimates based on the total installed capacity at the end of the year and may differ from official photovoltaic production data in some countries.

However, it is stated that they can be considered as indicative numbers that allow comparison between countries without reflecting official data.

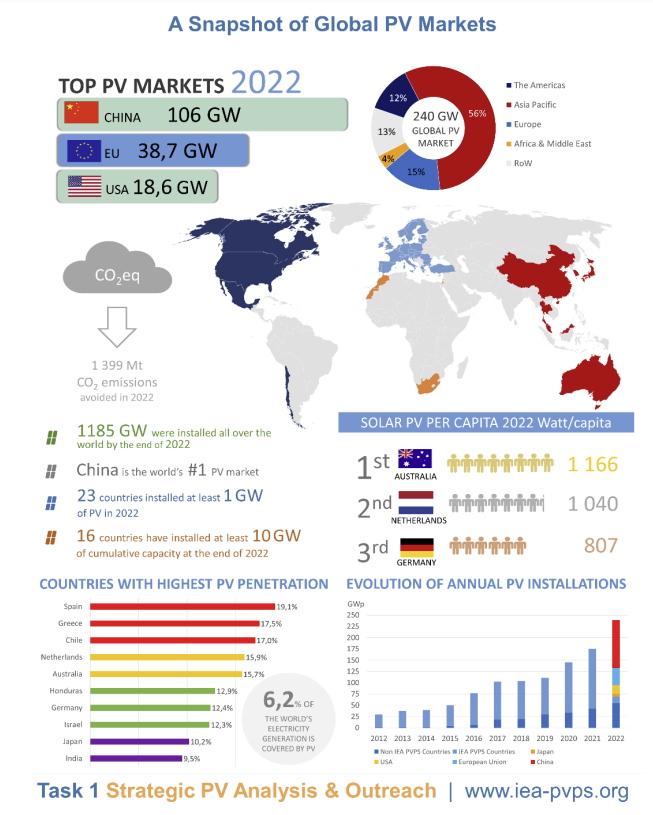

It is also worth noting that in 2022, nine countries recorded a PV infiltration rate of more than 10%, compared to just seven in the previous year. The authors of the report also point out that high infiltration rates are not limited only to countries with low consumption or intense sunlight, as Germany and India are among the top countries in terms of penetration rate, as shown in the chart below.

On the contrary, the increasing installed power of photovoltaic systems is the key element that enables solar systems to meet the growing energy demand. The two main markets, namely China with 6.5 percent and Europe with 8.8 percent, confirm this.

Overall, the contribution of photovoltaics to electricity is estimated at 6.2% worldwide.

An additional element to be emphasized is the importance of tenders for the development of the sector. According to the results of the report, tenders will continue to be the main driving force for utility scale solar systems in 2022, despite rising electricity prices. This led to more electricity purchase contracts (PPAs) or the choice of “merchant PV”.

As regards “merchant PV”, according to the report, this practice is growing steadily as investors seek to exploit the high prices of electricity on the market, thus avoiding tender-related restrictions (limited time, restrictive terms, insufficient quantity for auction, etc.) or as the only alternative when existing support schemes have been abolished.

Finally, it is worth mentioning that the global photovoltaic market is estimated to reach 240 GW by the end of 2022, with China having the largest market share with 106 GW, followed by the European Union with 38,7 GW and the United States with 18,6 GW, as shown in the following review for the past year.

{kind=link}